Labor or cost or productivity?

Welcome to another edition of SFTW. SFTW is the free version of “Software is Feeding the World” and includes previews only.

Happenings

- AgTech Alchemy is going to Seattle! Join the AgTech Alchemy crew of Sachi Desai, Walt Duflock, and I in partnership with the Gates Foundation at the Gates Foundation Discovery center on May 19th. You can register for the free event here.

- SFTW will move from Substack to a new hosting platform and newsletter service managed by Ghost. The move will happen over the next two weeks. I will try my best to reduce interruption. Emails will come from sftw@ghost.io or rhishi@rhishipethe.com. Ghost is an open-source product. I like their open source ethos and with the difference in take rate, Ghost is a more economical option.

- Over the last few weeks, I have started offering corporate subscriptions to different organizations. A corporate subscription comes with a significant discount, full access to SFTW Plus and is paid for by your organization, typically through their training and education budgets. If you would like to sign up your organization for a corporate subscription program, just reply to this email.

Build Less, Scale Faster: The Rise of White-Label Platforms

Ag leaders aren’t asking “Can we build it?”—they’re asking “Should we?” White-labeled platforms are helping agribusinesses move faster and deliver on strategy while staying focused. From carbon tracking to digital agronomy, e-commerce, and lab insights, leaders are choosing to scale through their brand, not by building new tech stacks. Customers don’t care who built it—they care that it works. With white-labeled tech, you can go to market fast with your logo, your workflows, and our managed infrastructure behind the scenes.

Labor or cost or productivity problem?

We were in a sweet potato packing house in Merced county in California. I was with the sweet potato farm owner and operator observing the sorting and packing operations, before sweet potatoes got shipped out to their fresh market customers.

The owner was talking with the packing house operations manager about hiring. They were looking to hire 2 new people for the upcoming season, but they had received 120 applications! The owner told the operations manager to stop taking applications, as they could not handle so many applicants.

One of my friends who works for an AgTech company was looking to hire a junior level product manager. She got more than 250 applications for one role. It was not straightforward to handle so many applications.

The unemployment rate in the US is at 4.2% and so it is not very high. I understand these are just two data points, but if we look at these data points, is there really a labor problem in California agriculture?

All of you have read about the many stories about the problem of labor in California. But the real problem is often with the cost of labor and the productivity of labor. Due to policy changes, and other factors, the cost of labor has gone up significantly.

It is important to understand this difference.

This is an important distinction to remember, especially for startups who are building robotics or automation solutions. This is true whether this is happening in California, the mid-west or any other part of the world.

If you think the problem to solve is the availability of labor, then you would think about building automation and autonomy solutions which strictly eliminate labor from the operation. Oftentimes, eliminating labor is not a good solution, if you are not having a positive impact on productivity, or reduction in operational risk, or quality of the product.

How can this difference show up in your solution?

Let us continue with the example of sweet potatoes. The cost of harvest using human labor is close to 50% of the total production cost for sweet potatoes. So if you were thinking about just eliminating human labor, an automated sweet potato harvester should work.

Automated Sweet Potato Harvester, Merced County, California (Photo by Rhishi Pethe)

But the problem is a bit more nuanced. The first question to ask is what is the market destination for your sweet potatoes. The requirements for the quality of sweet potato are different if you are selling the product to a fresh market vs. for processing.

Fresh market demand requires no to limited damage to skin and the right size to command a reasonable price. Fresh markets demand selectivity, gentle handling, and cosmetic perfection. Processing demand can accept sweet potatoes with damaged skin, odd shapes etc.

Today completely automated sweet potato harvesters exist. They can replace the entire hand sorting crew (except the tractor driver) and so as a startup if you think the problem you are trying to solve is labor, then you might think you have a good solution.

But if the market destination is a fresh market, then the automated sweet potato harvester does not work as it damages the skin of the sweet potatoes, reduces its shelf life, and so makes it difficult to sell in the fresh market.

So even though you have solved a labor problem, you have not really solved the business problem and so you don’t have a working product for that particular use case.

Let us take the example of Advanced Farm which did robotic apple harvesting and also ventured in strawberry harvesting. Advanced Farm had shut down in 2023, but their assets were picked up by CNH last year. By some measure, Advanced Farm was able to pick apples successfully without any human labor. In a recent article, Kyle Cobb, CEO of Advanced.Farm said the following

During our in-field testing in 2024, we picked hundreds of thousands of apples for leading growers in Washington. We did this with a single prototype machine that demonstrated an average pick rate of 2,500 apples per hour (three times faster than a human) while handling fruit just as gently as a human would. Our advances this past season in speed, reliability, and postharvest handling have proven to be important as we move to engaging growers across many more acres in 2025.

It is not enough to just compare the speed of the robot to a human, and the quality at which you are doing it, you also need to compare the cost of using the robot vs. cost of using humans for doing the same operation. Because at the end of the day, it is important that an alternate solution is cost-efficient compared to the existing alternative, without sacrificing productivity and quality needs for the particular operation.

For example, the case of baby carrots is a very interesting innovation, both from a consumer product perspective, as well as a farming operation perspective. Baby carrots are healthy and great for snacking.

But baby carrots are not some special type of carrot. They are regular carrots which are cut and processed. The baby carrots are cut from regular full carrots which didn’t have enough demand for the fresh market full carrots or their quality was such that you could not sell them in the fresh market full carrot segment.

So next time someone mentions there is a labor problem or they are solving a labor problem, you need to drill into whether they are solving a labor availability problem, a labor cost problem, a productivity problem or a product quality problem.

AI for food is health through molecule discovery

There has been significant hype about the use of GenAI in food and agriculture. I mean, yours truly has been feeding the hype through part 1 of the GenAI at the FarmGate report with examples from Bayer, Digital Green, Traive, and Kissan AI.

Everyone and their brother has been thinking about or coming out with initiatives for using GenAI. Most of these initiatives have been in the realm of using a chat bot to help with product discovery, customer support, or helping employees access information in an easier fashion.

Due to this, it is great to see the use of traditional AI for non-chat bot type uses.

For example, Brightseed has partnered with Haleon for small molecule discovery using AI.

Brightseed is the bioactives company on a mission to illuminate nature to restore human health. Brightseed discovers bioactive compounds in nature with its Forager® AI platform and develops novel, efficacious ingredients for food & beverage, specialized nutrition and consumer health companies.

Bioactives are compounds that interact with living tissue components and produce a positive effect on health.

From agricultural crops to specialized ingredients to pharmaceuticals, we are committed to advancing health by building an ecosystem that delivers the benefits of bioactives to consumers.

Over the years, Brightseed has built a huge database of plant-based compounds associated with biological targets. Their AI platform predicts how untapped components might provide health benefits which are specific and they understand how to source and produce them at commercial scale.

Haleon’s brands include Advil, Panadol, Theraflu, and Centrum, and a portfolio across oral health, pain relief, respiratory health, digestive health, and vitamins, minerals & supplements.

Brightseed is providing its Forager AI platform using a subscription model to Haleon.

This story is interesting as it is an example of potential cross industry collaboration, and the use of AI to expand the search space for solutions.

Growers Edge raises $ 25 million

Agrifintech player Growers Edge raised $ 25 million recently.

Growers Edge, a FinTech company focused on the agriculture sector, has raised $25m in a new funding round to scale its innovative financial services tailored to ag retailers, manufacturers, and lenders.

The round was co-led by S2G Investments, Cibus Capital, and Lowercarbon Capital. Additional backing came from Otter Creek, iSelect, and Jeff Ubben, the founder of ValueAct Capital.

Growers Edge offers a suite of financial tools designed to reduce risk and encourage innovation in farming. Its offerings include a Crop Plan Warranty Program, land and climate intelligence tools, digital mortgage lending products, and input lending solutions.

The company partners directly with manufacturers, retailers, and industry groups to help growers adopt innovative practices with confidence, and has worked with five of the top ten largest ag retailers and leading organizations, including Nutrien, PepsiCo, Mondelez, Helena Agri-Enterprises, and The Nature Conservancy.

Based on information from some sources, this was a significant down round, and which probably wiped out many of the early investors.

Growers Edge had raised $ 8 M in Series A in 2017 from Finistere Ventures and S2G, followed by a $ 40 million Series B in 2020 led by S2G, Cox Enterprises, Skyline Global and Bunge Ventures. In 2023, they did a B-extension for $ 15 million and did a pivot towards a full-stack fintech platform to service retailers and banks, by going beyond only warranty programs.

Their cap-table blends strategic investors, generalist growth funds, and climate investors. It is to be seen if it positions the company to monetize decarbonization incentives and traditional working capital flows for inputs etc.

Growers Edge strategy has evolved over the years. They started off with a data marketplace and benchmarking tools, which proved difficult to monetize based solely on insights. During the pandemic years, they added warranty backed crop plans to increase input spend while de-risking new technology.

The ZIRP period and crazy valuations didn’t do any favors to Growers Edge as they transitioned to a full service agri-fintech platform under one roof.

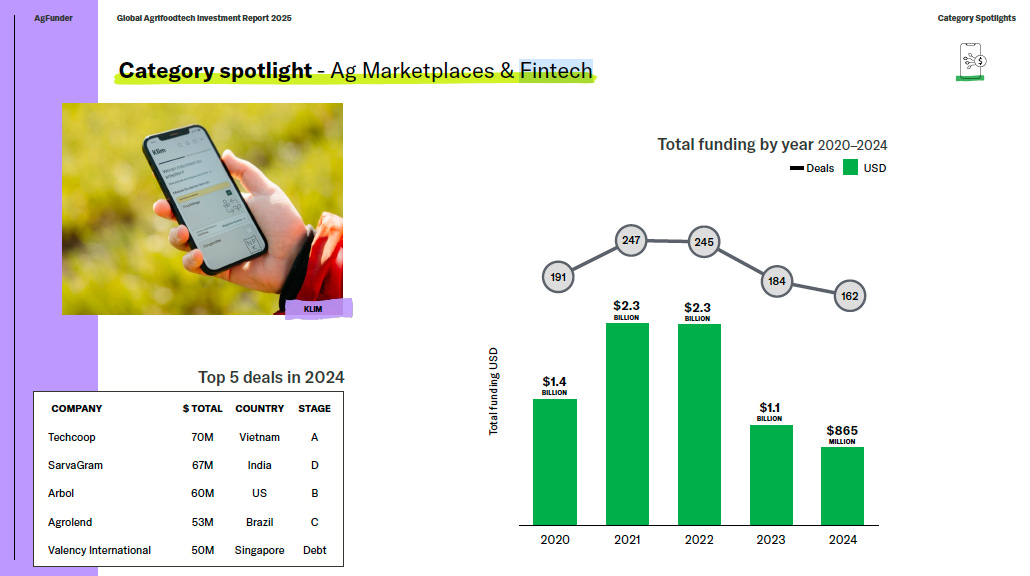

VC funding has slid in the last few years for AgriFoodTech, and the agrifintech category also slid by 23% (between 2023 and 2024), with developing markets getting a significant boost, led by India and Brazil, which showed the appetite for asset light credit models.

Image from AgFunder Global Agrifoodtech investment report for 2025

Growers Edge has some tailwinds going for it due to the US farm-debt cycle and the quantity of variable-rate operating loans due in 2025-2026. With the uncertainty in commodity markets due to tariffs, farmers might struggle to find markets to sell their products, prompting challenges on the input sides. This will require more and more retailers to have embedded finance capabilities to offer to their customers.

It is expected that in the current economic environment with agriculture and AgTech being on the down cycle, there will be significant consolidation on the agriculture retail side. Retail consolidation could see Growers Edge snapped up by a crop‑input major seeking fintech capabilities or by a re-insurer to gain access to technology and some new channels.